Thelander PC Digest: May 2026

The Option Pool Paradox: Why Higher Valuations Don’t Always Pay Off

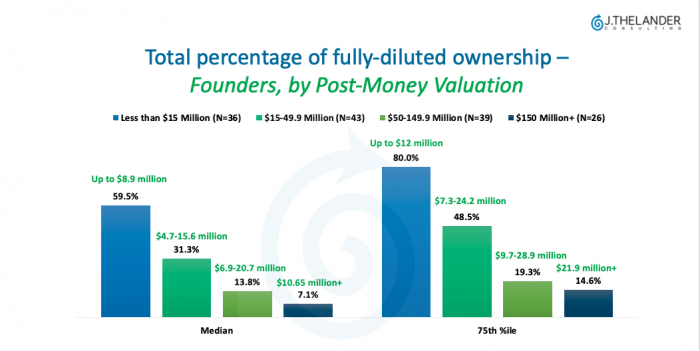

We’re taking last week’s analysis one step further: what do those different option pool sizes actually mean in dollar terms?

The short answer is that a higher valuation doesn’t automatically translate into a better outcome for founders. A smaller slice of a bigger pie can — and sometimes does — mean less money in your pocket.

Using the chart above from the Thelander Option Pool Report (available on the Thelander Platform), we looked at the median and 75th percentile of total percentage of fully-diluted ownership for founder across valuation tiers, then multiplied those percentages by the corresponding valuation ranges to calculate dollar equivalents. A smaller slice of a bigger pie can – and sometimes does – mean less money in the your pocket.

Then, we took the percentages and multiplied them by the valuation range — because the valuation is how much the total option pool is theoretically worth — which corresponds to the green labels on top of the percentiles.

What the data shows

When you look at the dollar equivalent ranges for founders across valuation tiers, the picture is more complicated than it might appear.

At the 75th percentile, founders at companies valued between $15M and $49.9M are looking at a dollar equivalent range of $7.3M to $24.2M.

At the median option pool size for the next valuation tier ($50M–$149.9M), that range is actually lower at $6.9M–$20.7M.

In other words, the shares of a founder at the 75th percentile for a $30M company may be worth more than those of a founder at a $75M company if that $75M founder’s option pool is closer to the median for the corresponding level.

This dynamic holds at higher valuations too.

At $150M+, the median founder holds just 7.1% of fully-diluted ownership — down from 59.5% at the sub-$15M stage.

Even at the 75th percentile, ownership drops to 14.6% at $150M+.

The dollar equivalents do increase at the top end ($10.65M at the median, $21.9M+ at the 75th percentile for $150M+ companies), but the path there is not guaranteed — and it depends heavily on how the option pool was structured at every stage along the way.

Why does this happen?

As valuation increases, the percentage of the option pool going to founders tends to decrease relatively quickly. At higher valuations, that dilution can outpace the gains from a larger pie. The result: founders who don’t actively manage their founder equity and additional equity for holding an executive position (more on that here) can find themselves holding shares that are worth less in real dollar terms than they would have been at an earlier stage.

This is why having access to real-time market data throughout the lifecycle of a company isn’t just a fundraising exercise — it’s an ongoing discipline. The decisions made at each round of financing compound, and by the time a company reaches later-stage valuations, the structure of the option pool is largely locked in.

What’s the bottom line?

Higher valuations generally correspond to higher dollar equivalent ranges overall — but they do not always make up for the smaller portion of the option pool going to founders.

Thelander is the only compensation intelligence firm to cover both sides of the private company compensation equation, from investment firms to founders — and to do so globally. A single point of truth. To see how your current mix of cash and equity compensation compare to market and to download the Option Pool Participant Report, complete the Thelander Private Company Compensation Survey today.

Tags: Private Company